1. Determine a method for aligning performance-based budgeting with the current budget cycle and process and think about messaging the changes internally early in the process.

Since cities already have budget processes that have been in place for decades, ensuring that the transition to performance-based budgeting is as logistically seamless as possible is important for successful adoption and implementation. Aligning the new process with existing schedules and procedures can make it easier for employees to adjust to performance-based budgeting. This also helps ensure that employees focus on progress toward goals--the crux of performance-based budgeting--rather than logistical changes.

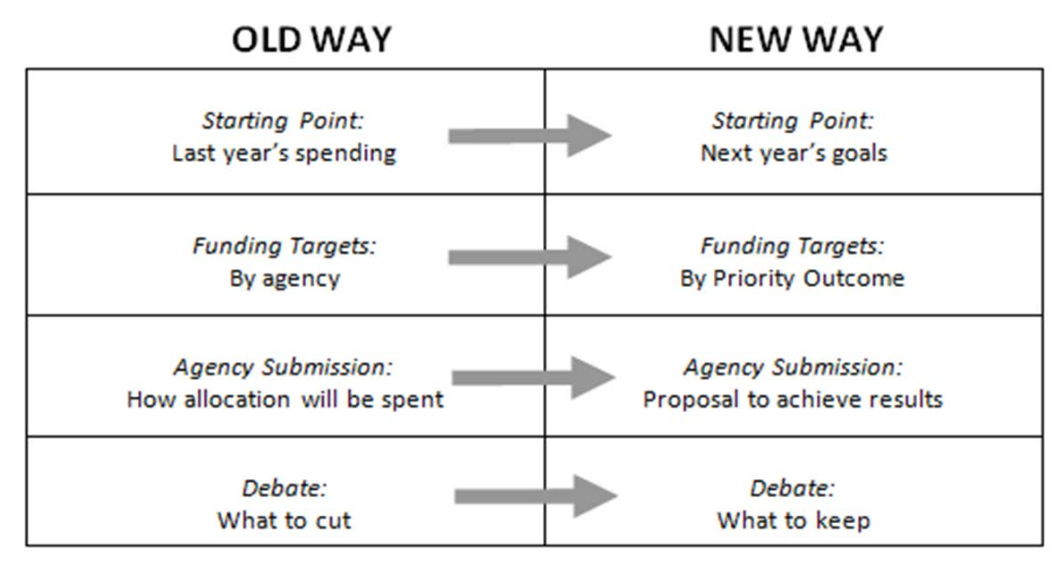

In 2011, Baltimore, MD, was very clear in messaging the move to performance-based budgeting to city staff and officials and aligning this process to its previous budgeting schedule. This required reframing the budget conversation from considering last year’s spending on agency goals and debating what to cut to focusing on next year’s strategic goals for citywide priorities and debating what is worth keeping in the budget. In Baltimore, performance-based budgeting is connected to its CitiStat program, strategic plan, and agency performance agreements and aligns with the city’s goal of being a performance-based city so it seemed like a natural addition to city staff.

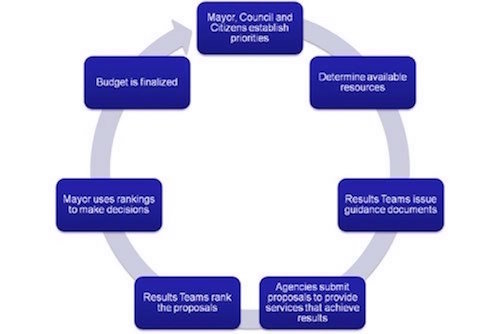

Providing timelines and coaching to explain how performance management fits in with the existing budget process is the first step to ensuring that departments and agencies understand and use performance-based budgeting effectively. Baltimore, like many cities, has historically had a long and detailed process for developing and submitting agency budgets, beginning in September and lasting through July when the budget is adopted. To make it easier for agencies to align their budget requests with the performance-based budgeting and performance metrics, Baltimore’s budget office includes step-by-step guidance for agencies detailing the mayor’s priority outcomes (see Appendix A for examples of citywide priorities in performance-based budgeting), informed by the annual citizen survey, and indicators of emphasis for the fiscal year budget process. By clearly defining the budgeting expectations and process up front, the city ensured staff participation and buy-in, reconciling a $500 million budget deficit in four fiscal years.

Source: http://bbmr.baltimorecity.gov/OutcomeBudgeting/AboutOutcomeBudgeting.aspx